can non-US citizens buy property in America

its complete guide for Non Us citizens how to buy property in America. written by muhamamd qaisar on www.alazizpropertypk.com . some expert helps us to prepare this guidlines for overseas .

Can non-US citizens buy property in America? Absolutely yes. Learn visa requirements, ITIN mortgage, FIRPTA tax rules, and step-by-step buying process for foreign nationals in 2026.

Published by Alazizpropertypk.com | May 2026 | Category: US Property · Foreign Buyers · Overseas Guide

The Short Answer .Yes. But Let’s Talk About What That Actually Means

Every week, thousands of people around the world type some version of this question into Google. A student on an F-1 visa wonders if she can put her savings into a small apartment near her university. An H1B worker in Texas has been renting for four years and starts thinking it might be time to build something of his own. A Pakistani family in New Jersey wants to understand whether their parents, who just arrived on a visitor visa, could be added to a property title.

The question feels complicated because people assume American property law must have some wall built around it for foreigners. The reality is actually more welcoming than most people expect. The United States does not have a federal law that bars non citizens from owning real estate. That door is open. What matters is understanding the specific rules that apply to your particular situation your visa type, your tax status, your financing options, and your long-term plans.

This guide walks through all of it in plain language. No unnecessary legal jargon, no vague generalities. Just a clear picture of what foreign nationals can do, what the process looks like in 2026, and what the most important things to watch out for are.

Note:

This guide provides general information for educational purposes. Laws and lending policies change. Always consult a licensed US real estate attorney and a qualified tax professional before making any property purchase decisions.

Who Will Counts as a Non-US Citizen When It Comes to Property?

Before going any further, it helps to understand how the term “NON-US citizen” breaks down in practice, because your specific status shapes almost every part of the buying process.

Permanent Residents (Green Card Holders)

If you hold a green card, you are a lawful permanent resident of the United States of America. From a property buying standpoint, your situation is almost identical to that of a US Citizen. You can get a conventional mortgage, apply for FHA loans in many cases, and purchase property in any state without restriction. The main difference shows up at tax time, particularly if you sell and need to deal with capital gains , but for the purpose of actually buying a home, permanent residents face essentially no additional hurdles.

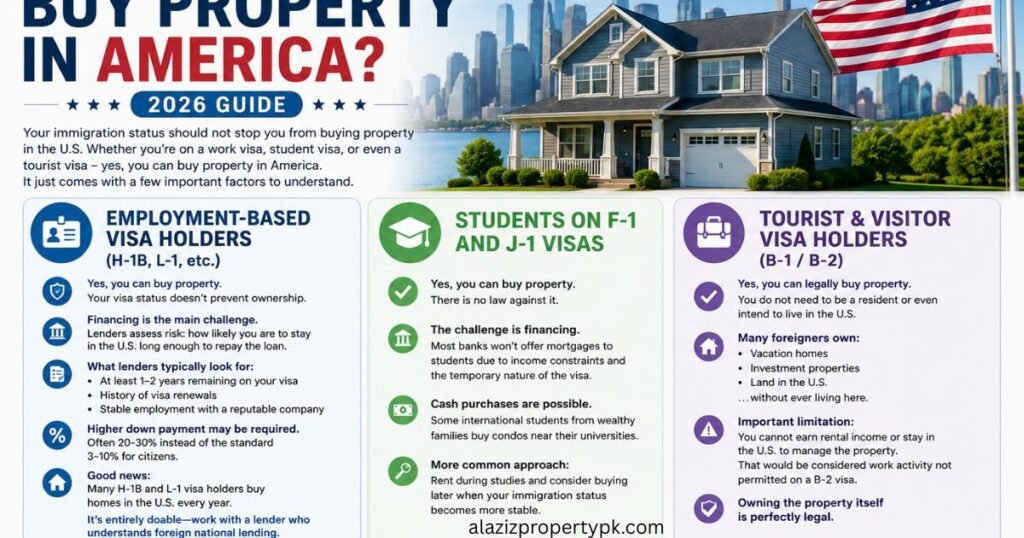

Work Visa Holders .(H-1B and L-1 visa holders )

This is the category that generates the most questions. Many skilled professionals working in the US on employment based visas wonder whether their temporary immigration status should stop them from buying property and get nationality. The answer is no . it should not stop you, though it does add a layer of complexity to the financing side of things.

Banks and mortgage lenders look at visa holders through the eyes of risk. They want to know ,How likely is this person to remain in the US long enough to repay this loan? For that reason, most conventional lenders prefer to see at least one to two years remaining on your current visa, a history of visa renewals, and employment with a stable company. Some lenders also require a larger down payment from visa holders compared to citizens .typically 20 to 30 percent rather than the standard 3 to 10 percent.

That said, many H-1B and L-1 visa holders successfully purchase homes in the United States every year. It is entirely doable .it just requires working with a lender who understands foreign national lending rather than walking into the first bank you find.

Students on F-1 and J-1 Visas

Technically, even a student on an F-1 visa can buy property in the US. There is no law against it. The practical challenge is financing — most banks will not offer a mortgage to someone on a student visa, both because of income constraints and because of the temporary nature of the visa. Cash purchases are entirely possible, however. Some international students from wealthy families do purchase condominiums near their universities. The more common approach, though, is to rent during studies and consider purchasing later if immigration status changes to something more stable.

Tourist and Visitor Visa Holders (B-1 / B-2)

Yes, even someone on a tourist visa can legally purchase real estate in the United States. You are not required to be a resident or even have an intention to live in the US to own property here. Many foreign nationals own vacation homes, investment properties, or land in America without ever living here. What you cannot do on a tourist visa is earn rental income and stay in the country to manage the property ,That would cross into work activity not permitted on a B-2 visa. But owning the asset itself is perfectly legal. alazizpropertypk.com compile these information with the help of experts.

Undocumented Individualsn in usa

This is the category that carries the most uncertainty. There is no federal law explicitly prohibiting undocumented individuals from owning property. Some have successfully purchased homes using an Individual Taxpayer Identification Number (ITIN) rather than a Social Security Number. However, the financing is extremely difficult, legal exposure exists in certain states, and the broader immigration consequences of financial paper trails require very careful consideration. Anyone in this situation should consult an immigration attorney before taking any steps.

What Documents Do You Actually Need to Buy Property in the USA?

One of the biggest misconceptions foreign buyers have is that they need a Social Security Number to purchase property in usa. You do not .Though having one makes the process considerably smoother. Here is what you typically need depending on your situation:

If You Have a Social Security Number

1.Valid government-issued ID

2.Passport or driver’s license

3. Social Security Number for credit checks and mortgage applications .

4.Proof of income . pay stubs, employment letter, and last two years of tax returns .

5.Bank statements for the past three to six months showing funds for down payment and closing costs .

6. Visa documents .current visa, I-94 record, and any previous visa renewals if applicable

If You Do Not Have a Social Security Number. Using an ITIN in America

An Individual Taxpayer Identification Number, or ITIN, is a tax processing number issued by the Internal Revenue Service to individuals who need to submit file US taxes but are not eligible for a Social Security Number. This includes many foreign nationals, non resident investors, and others outside the standard immigration channels.

An ITIN can be used to:

1.Purchase property in all 50 US states ,

2. Open a US bank account at certain banks .

3. File US tax returns and report rental income .

4.Apply for certain mortgage products through ITIN mortgage programs

ITIN mortgage programs exist specifically for foreign nationals and undocumented individuals who do not qualify for conventional financing. Interest rates on these products tend to be higher than standard mortgages, and down payment requirements are usually larger, but they represent a real pathway for buyers who otherwise have no financing options.

To apply for an ITIN, you complete IRS Form W-7 and submit it along with identification documents and a completed tax return. The process takes several weeks. Many tax professionals and CPAs assist with ITIN applications as a routine service.

For Cash Buyers

If you are purchasing without financing ,meaning you are paying the full purchase price in cash .The documentation requirements are significantly simpler. You will need proof of funds, a valid passport, and in most cases a source of funds letter explaining where the money came from. This source of funds requirement has become more rigorous in recent years as part of anti-money laundering regulations, particularly for high-value purchases.

Can Non Citizens Get a Mortgage in the United States?

This is the question that stops many foreign buyers in their tracks. The answer is yes .but the path to getting there looks different depending on who you are and what your immigration status is.

Conventional Mortgages for Visa Holders

Major banks and conventional lenders can offer mortgages to non-citizens who have a valid Social Security Number, documented US income, and a credit history in the United States. The challenge for many foreign nationals is that last part. credit history. If you arrived in the US two years ago and have been living here on a work visa but never opened a credit card or took out any form of credit, you may have zero US credit history even if your financial situation in your home country is excellent.

Building US credit takes time. The practical advice for anyone who plans to buy property in the US within the next few years is to start building credit immediately, open a secured credit card, pay it off in full every month, and let that history accumulate. Twelve to twenty-four months of clean credit history makes a significant difference in what lenders will offer you.

Foreign National Mortgage Programs

Several lenders in the United States have developed specific mortgage programs for foreign nationals. people who earn income outside the US and may not have a US credit history or Social Security Number. These programs are especially common in states like Florida, Texas, New York, and California where foreign investment in real estate is a significant part of the market.

Foreign national mortgage programs typically require:

1.A down payment of 25 to 40 percent of the purchase price.

2. Proof of income from your home country .

3.Pay stubs, tax returns, or business financials translated into English ,

4. A reference letter from your home country bank ,

5. Passport and visa documentation .

6.A US bank account with sufficient reserves .

7. Typically six to twelve months of mortgage payments

Interest rates on foreign national mortgages are usually half a percent to one full percent higher than standard mortgage rates, reflecting the additional perceived risk. That said, in a market where many properties generate strong rental income, the math can still work very favorably.

FIRPTA . The Tax Rule Every Foreign Property Buyer Must Understand

If there is one piece of US tax law that every foreign property owner absolutely needs to understand, it is FIRPTA. The Foreign Investment in Real Property Tax Act has been around since 1980, but it still catches people by surprise — usually at the worst possible moment, which is when they are trying to sell.

What FIRPTA Actually Does

FIRPTA is a withholding mechanism, not an additional tax. When a foreign person sells US real property, the buyer is required by law to withhold a portion of the purchase price and send it directly to the IRS. This withholding rate is currently 15 percent of the gross sale price . not the profit, but the entire sale price. alazizpropertypk.com will suggest you to learn about complete laws and follows.

So if you are a Pakistani national who bought a condo in Miami for $200,000 and later sells it for $300,000, the buyer must withhold $45,000 (15 percent of $300,000) and send it to the IRS. You would then file a US tax return, calculate your actual capital gains tax owed, and receive a refund of any amount withheld in excess of your actual tax liability. The withholding is not the final tax .It is more like a deposit held by the IRS until your return is filed.

Are There Any Exceptions to FIRPTA Withholding?

1.If the sale price is $300,000 or less and the buyer intends to use the property as a personal residence, the withholding rate drops to 0.

2. If the sale price is between $300,000 and $1,000,000 and the buyer intends to use it as a personal residence, the withholding rate is 10 percent rather than 15 percent .

3.If you obtain a withholding certificate from the IRS before closing, the withheld amount can be reduced

Working with a tax professional who handles international real estate transactions is strongly recommended for any foreign seller.

Best US States for Foreign Property Buyers in 2026

While any state in America allows foreign nationals to purchase property, certain states have emerged as particularly popular with international buyers.

1.Florida . No state income tax, warm climate, large international community, strong rental demand. Entry price: $250,000–$450,000

2.Texas .No state income tax, strong job market, lower costs than California or New York, fast-growing cities like Houston, Dallas, and Austin. Entry price: $220,000–$400,000

3.New York . Global financial hub, strong rental income potential, NYC properties hold value over time. Entry price: $400,000_$1M+

4.California . Large South Asian and Pakistani diaspora, tech economy, strong appreciation history. Entry price: $500,000–$1.2M.

5.Georgia . Lower entry prices, growing Atlanta metro, large international student population. Entry price: $200,000–$380,000.

6.Arizona . Affordable compared to the coasts, growing Phoenix market. Entry price: $280,000–$450,000.

For Pakistani nationals specifically, New Jersey, Texas, and Georgia tend to have the largest established Pakistani-American communities, which makes the practical experience of buying and settling much more navigable.

The Buying Process . Step by Step for Non-Citizens

1: Get Your Finances in Order First

Before you look at a single listing, understand your budget. If you are financing, get a mortgage pre-approval from a lender who works with foreign nationals. If you are paying cash, prepare a proof of funds letter from your bank. Also think through your currency situation — if your money is sitting in a Pakistani or other foreign bank account, understand the exchange rate dynamics and the most cost-effective way to transfer funds to the US.

2: Get Your ITIN If You Do Not Have an SSN

If you do not have a Social Security Number and intend to purchase property, apply for an ITIN early. The process takes several weeks and you will need it for tax-related paperwork at closing and for filing returns afterward.

3: Find a Real Estate Agent Who Understands Foreign Buyers

Not every real estate agent has experience working with non-citizen buyers. Ask specifically whether they have worked with international clients. In areas with large Pakistani or South Asian communities — parts of New Jersey, Houston, Dallas, the greater Atlanta area, and various California cities — there are realtors from within those communities who specialize in working with overseas buyers.

4: Make an Offer and Open Escrow

When you find a property, your agent submits an offer. If accepted, you enter the escrow period — typically 30 to 45 days — during which inspections are conducted, financing is finalized, and both parties prepare for closing.

5: Title Insurance and Closing

Title insurance protects you against any undisclosed liens or ownership disputes after purchase. At closing, you sign final documents, funds are transferred, and the deed is recorded in your name. If you cannot attend closing in person, a power of attorney arrangement allows someone to sign on your behalf — this is routine and well understood by US title companies.

6: Register with the IRS and Understand Your Ongoing Obligations

If you earn rental income from a US property, that income is subject to US federal income tax and must be reported annually. Property tax is paid to the local county or city government and varies significantly by location.

A Special Note for Pakistani Nationals Buying Property in the USA

The NICOP Advantage

Pakistani nationals living abroad can apply for the National Identity Card for Overseas Pakistanis. While it does not directly affect your ability to purchase US property, it significantly simplifies your dealings with Pakistani banks, property authorities, and the Federal Board of Revenue if you are managing investments in both countries simultaneously. that what alazizproperypk.com inform you.

Dual Investment Strategy

Many Pakistani americans pursue a dual investment approach. Building equity in the US market while simultaneously holding real estate in Pakistan. The logic is sound: your US property appreciates in dollar terms, while your Pakistani property benefits from structural demand and growth in Pakistan’s urban centers. When managed well, the two markets complement each other rather than compete for the same capital.

The United States and Pakistan have a tax treaty in place that provides some protection against double taxation for Pakistani nationals with US income or assets. It does not eliminate all obligations in both countries, but it provides credits and mechanisms to avoid paying full tax twice. A CPA familiar with both Pakistani and US tax law is genuinely worth the investment if you hold assets in both countries.

Frequently Asked Questions

Can I buy property in the US on a tourist visa? Yes. There is no law preventing someone on a tourist or visitor visa from purchasing real estate in the United States. The limitations are on what you can do with the property. you cannot live in it as a full-time resident without the appropriate immigration status. But owning the asset is entirely legal.

Do I need a US bank account to buy property? You do not legally require one, but in practice it makes the process significantly smoother. Most closing transactions involve wire transfers, and having a US account simplifies that considerably. Several major US banks allow non-residents to open accounts with a passport and foreign address.

Can I rent out a US property if I live outside the country? Yes. Many foreign nationals own rental properties in the US and manage them from abroad through property management companies. The rental income must be reported to the IRS and is subject to US federal income tax, even if you are not physically in the country.

What happens to my US property if my visa is not renewed? Your property ownership does not depend on your visa status. If your visa expires and you leave the United States, you still own your property. You can continue to rent it out, hire a management company, and sell it when you choose. The property does not revert to the government based on your immigration status.

Is there any restriction on how many properties a foreign national can own in the USA? No federal restriction exists on the number of properties a foreign national can own. Some states have recently passed narrow legislation restricting certain foreign nationals from purchasing agricultural land or property near military installations, but for most buyers interested in residential or investment property in major cities, these laws do not apply.

What is the safest way to transfer large sums from abroad to buy US property? Use regulated, documented channels only — international wire transfers from your home bank, or established services like Wise or OFX. Keep complete records of every transfer, including confirmation numbers and exchange rates applied. These records are important for both US and home-country tax compliance.

Closing Thoughts

The United States remains one of the most open real estate markets in the world for foreign buyers. Not holding a US passport or green card does not close this market to you .it simply means you need to understand the specific rules and processes that apply to your situation.

The most important things to remember: understand your visa category and what it means for financing, get your ITIN early if you do not have an SSN, work with professionals who have genuine experience with foreign national transactions, understand FIRPTA before you plan to sell, and keep documentation of every financial transaction from the very first dollar you move.

For Pakistani nationals in particular, 2026 is a genuinely interesting moment to be thinking about US property. The Pakistani diaspora in America is larger and more financially established than ever, the tools for cross-border investment management have never been better, and the dual investment strategy of holding assets in both markets is something more and more people are successfully executing.

Take your time, build your team of advisors carefully, and make decisions based on documented facts. The opportunity is real .and it is not going anywhere.

Alazizpripertypk.com covers real estate investment for both Pakistani and international audiences. Visit alazizpropertypk.com for more guides.

Alazizpropertpk.com is a modern real estate and cryptocurrency-focused platform dedicated to providing secure, innovative, and reliable investment opportunities. We specialize in property buying, selling, investment consultancy, and crypto-integrated real estate solutions. Our goal is to bridge the gap between traditional real estate and the digital financial world by offering transparent services, expert guidance, and smart investment strategies for local and overseas clients. With a commitment to trust, innovation, and customer satisfaction, Al Aziz Property PK is helping shape the future of real estate in World.